A consumer fills out a mortgage application on Tuesday morning. Their credit is pulled at 10:47 AM. By Wednesday afternoon, they’ve already chosen a lender, but it might not be you. In consumer lending, sometimes the window between “in-market” and “already decided” can be measured in hours, not days.

The lenders who win aren’t necessarily offering better rates.

They’re simply getting there first, with the financial product or offer, at exactly the moment the borrower is making their decision.

Credit trigger marketing offers a powerful advantage for consumer lending organizations looking to outpace the competition.

Sometimes referred to as “trigger lists,” this strategy uses real-time credit bureau data to identify consumers who meet a lender’s specific targeting criteria. These criteria can include recent credit inquiries, overall credit rating, outstanding balances on credit cards or loans, total debt, credit utilization, and the borrower’s credit mix. By honing in on consumers at the precise moment they’re demonstrating intent or financial movement, lenders can engage with offers that are timely, relevant, and far more likely to convert.

The Problem with Traditional Marketing Lists

In financial services, a so-called “fresh” direct mail list might still be 30, 60, or even 90 days old.

That means by the time your credit offer reaches the mailbox, the consumer may have already chosen a lender or moved on entirely.

This delay is one of the main reasons traditional credit-driven campaigns, such as prescreened credit card or loan offers, tend to produce average response rates of just 1 to 2 percent.

Even more timely trigger-based programs, which are sent shortly after a credit inquiry, typically see response rates in the range of 2 to 4 percent. Campaigns targeting your existing customer base often perform better, with cross-sell or upsell efforts reaching response rates of 3 to 6 percent or more. But even then, many marketers find themselves struggling to stand out.

The core issue is that traditional lists are answering the wrong question. They show who qualified for credit weeks or months ago, rather than identifying who is actively shopping today. When you rely on outdated or static data, you’re limiting your ability to act in real time and capture real demand.

If the goal is to outperform the industry average, marketers need more than names and credit scores. They need signals that reflect current behavior, recent activity, and real intent so they can reach people who are ready to take action right now.

What Makes Credit Triggers Different

Most marketing lists tell you what happened weeks or months ago. Credit triggers, on the other hand, provide a real-time view into a consumer’s financial journey—so you can reach them while they’re actively considering a financial decision, not after the fact.

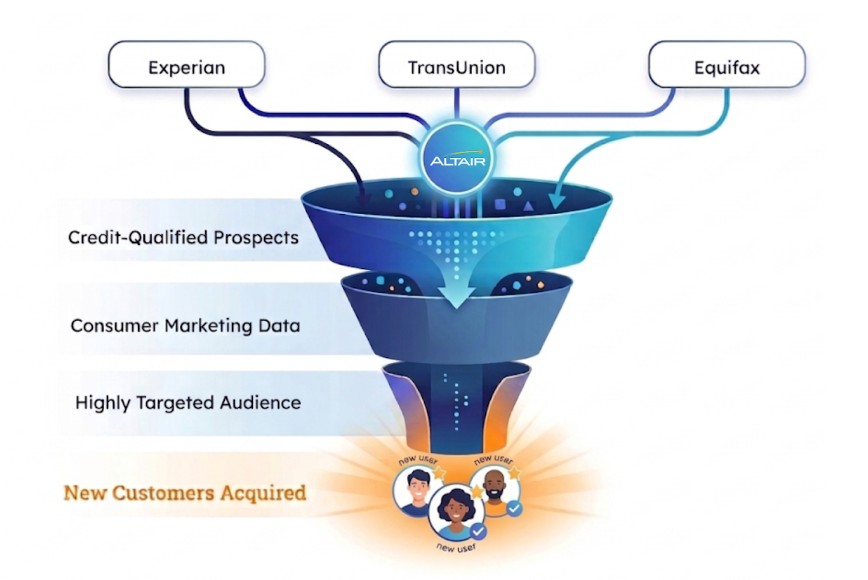

While credit inquiries are among the strongest signals of in-market intent, they’re only part of the picture. Altair’s Monitor360 gives you access to over 100 credit and consumer signals, including:

Real-Time Credit Inquiries

When a consumer applies for a mortgage, auto loan, personal loan, or credit card, that inquiry can be detected within minutes, allowing you to deliver offers at the exact moment interest peaks.

Credit Score Migration

If a consumer’s score improves, you can proactively offer better terms or upsell them to premium products—before a competitor does.

Refinance and Cash-Out Eligibility

Monitor borrowers who now qualify for refinancing or cash-out based on recent credit changes or property data.

PMI Removal and Specialty Alerts

Identify homeowners who now qualify to drop PMI or meet other niche thresholds valuable for targeting.

This depth of monitoring creates key advantages:

Timing

Alerts are delivered in near real time—within 24 hours or even minutes—so you can be first in the mailbox, inbox, or ad stream.

Intent

These are not generic marketing segments. They reflect real consumer behavior tied to major financial decisions.

Qualification

Triggers include pre-screening based on your lending criteria, so you’re reaching people who are both interested and eligible.

Coverage

With Monitor360’s tri-bureau approach, you unlock broader visibility and can reach up to 50% more qualified prospects than single-bureau options.

By blending credit and real-world life signals, credit triggers move you from reactive campaigns to proactive, always-on performance marketing. Whether you’re focused on acquisition, cross-sell, or churn prevention, these triggers ensure you reach the right customer at the right moment—with the right message.

The Response Rate Reality

The data on trigger-based marketing versus traditional approaches is compelling.

Direct mail campaigns using credit trigger data consistently outperform batch-and-blast approaches. Real-world results show even more dramatic improvements:

- Altair clients using Monitor360 for VA loan triggers saw a 38% lift in conversions

- Targeting new homeowners faster delivered 3.5X campaign response rates

- One agency generated $1.2 million in new revenue by implementing always-on trigger campaigns for one of their clients

Why the significant difference? According to research, the first 24-48 hours after a credit inquiry are when consumers are most likely to be approached by competing lenders, and most likely to make their decision. Lenders who respond within this window capture attention before the borrower commits elsewhere.

Beyond Credit: The Complete Picture

Traditional credit triggers only tell part of the story. A credit inquiry shows someone is shopping, but it doesn’t reveal why they’re shopping or what else is happening in their life.

This is where modern monitoring solutions like Monitor360 create an unfair advantage. By combining credit triggers with consumer data signals, you get context that dramatically improves targeting precision:

Life Events

New marriage, divorce, new child—major life moments that drive borrowing behavior

Property Signals

Pre-movers listing homes, updated home values showing equity opportunities, property transfers indicating new homeowners

Shopping Behavior

Online mortgage shopping activity, digital research signals showing active consideration

Portfolio Risk

Credit score migrations, utilization spikes, competitor inquiries that indicate churn risk

Traditional Credit Data vs. Credit Trigger Marketing

| Traditional Credit Data Pulls | Credit Trigger Data + Consumer Data | |

| Data Timing | Batch files delivered monthly or quarterly; data can be 30-90 days old at time of use | Near real-time alerts (<24 hours, some within moments) when specific credit or life events occur |

| Cost Structure | Pay for entire file regardless of whether the person is in-market; cost per thousand (CPM) pricing | Pay only for qualified credit and/or non-credit triggers; event-based pricing for in-market consumers |

| Targeting Precision | Broad audience modeling based on credit characteristics and demographics | Laser-focused on consumers actively shopping for credit products (mortgage inquiries, new auto loans, etc.) or experiencing life events, like moving |

| Response Rates | Industry average 0.5-2% depending on offer and audience quality | Typically 2-5x higher due to timely, relevant outreach to in-market consumers |

| Best Use Case | Traditional acquisition programs at scale, portfolio reviews, annual promotions, retention programs | Competitive acquisition, life event marketing, cross-sell opportunities, balance transfer offers |

| Campaign Flexibility | Set audience at time of pull; requires new pull to update targeting | Continuous flow of qualified prospects; always-on campaign capability |

Credit data tells you who qualifies, but consumer and behavioral data shows who’s actually interested—and why.

Want to learn more? Download Altair’s “Half Picture Problem” to learn how credit + consumer data together can unlock a new level of marketing performance.

How Trigger Programs Actually Work

Implementing a credit trigger program used to require complex data vendor relationships and technical infrastructure. Modern platforms have simplified the process significantly.

Here’s how Monitor360 works:

1. Set Your Criteria

Define your ideal borrower profile—credit score ranges, loan types, geographic areas, and specific trigger types you want to monitor.

2. Automated Monitoring

The system monitors credit inquiries and other signals across all three major credit bureaus plus consumer data sources—over 100 different trigger types in total.

3. Real-Time Delivery

When a consumer matches your criteria, you receive the alert within 24 hours (often within moments for certain trigger types). Integration options include API, SFTP, or platform delivery.

4. Instant Activation

Trigger data can feed directly into your marketing automation, CRM, or be pulled on-demand from the DataCloud platform for same-day campaign launches.

The key is that this happens continuously, automatically, in the background. You’re not manually pulling lists or waiting for file transfers. Opportunities flow to you as they happen.

Multi-Channel Deployment for Maximum Impact

The most effective trigger strategies don’t rely on a single channel. Adopting a multichannel approach has shown a roughly 39% incremental lift in household response rates.

Here’s how leading lenders deploy trigger data:

Direct Mail

Physical mail pieces still command trust in financial services. Response rates range from 2% to over 5% depending on targeting and message quality. Direct mail is particularly effective for longer consideration products like mortgages and HELOCs.

For time-sensitive triggers, email enables immediate outreach with dynamic rate quotes and loan scenarios tailored to the trigger type.

SMS

With a 98% open rate and most messages read within three minutes, SMS is ideal for urgent alerts like rate changes or time-sensitive offers.

Digital Display

Deliver tailored brand messages to high-intent audiences across display networks and social platforms, supporting direct mail and email efforts throughout the buyer journey.

The channel mix should match the urgency of the trigger and your product type. Mortgage triggers might deploy via direct mail with email follow-up. Credit card triggers might start with SMS and email for faster response.

The Compliance Reality

Credit trigger marketing operates under strict Fair Credit Reporting Act (FCRA) regulations. Any lender using credit data for marketing must make a “firm offer of credit” to the consumer. You can’t just browse credit files for leads without being prepared to extend credit.

This requirement actually works in marketers’ favor. It ensures you’re only reaching consumers who genuinely qualify for your products, reducing wasted spend on unqualified prospects.

Modern trigger platforms like Monitor360 have FCRA compliance built in, with audit trails and permissible purpose controls that ensure your campaigns meet regulatory requirements without slowing you down. The system handles the compliance complexity so marketing teams can focus on campaign performance.

The Changing Landscape

The trigger lead market is evolving. The Homebuyers Privacy Protection Act, signed into law with implementation beginning March 5, 2026, restricts how credit bureaus can sell consumer credit inquiry data. This is a meaningful shift, and it’s worth understanding what’s gained and what’s lost.

Banning the barrage of unsolicited calls to borrowers who just applied for a mortgage? That was a real problem, and the industry largely agrees the change was overdue.

But the law doesn’t just restrict recent trigger solicitations—it prohibits mortgage triggers and prescreens from being used in perpetuity on anyone who triggered on a mortgage in the past. And that’s where the unintended consequences begin to surface.

Consider this: 22% of mortgage triggers convert to a closed loan within 90 days. That means 78% of consumers who applied for a mortgage didn’t or couldn’t get one. Before this bill, lenders could monitor those consumers. When their credit score improved, their debt load dropped, or they finally crossed the threshold into mortgage-eligible. That monitoring is now gone—permanently.

The borrowers most affected aren’t the well-resourced consumers with established banking relationships. They’ll get found. It’s the first-time homebuyer who doesn’t know where to start, the underserved consumer who was 18 months away from qualifying, or the borrower in a community where homeownership rates are already lagging.

These are the people who benefited most from being identified when they were finally ready—and that tool has been permanently eliminated.

That said, the mortgage industry has always adapted to regulatory shifts, and this one is already driving innovation. What this means for marketers:

Own your data

Your existing customer database is now your most strategic asset. With external mortgage trigger pipelines permanently restricted, tools like Monitor360’s portfolio monitoring become your primary mechanism for identifying when current customers are shopping for new credit—giving you a heads-up to retain business before they leave.

Quality over quantity

The days of buying massive trigger lead lists sold to dozens of lenders simultaneously are ending. The future belongs to more exclusive, better-targeted trigger programs with stronger compliance frameworks.

Focus on value

With consumers receiving fewer unsolicited trigger-based offers, the ones who do receive your outreach will be more receptive—if your offer is genuinely relevant and well-timed.

This regulatory evolution doesn’t eliminate trigger marketing for non-mortgage products, and it doesn’t reduce the importance of real-time data. If anything, it raises the bar—pushing lenders toward the kind of sophisticated, compliant, consumer-beneficial programs that deliver real value to both sides of the transaction.

The Next Phase of Mortgage Marketing

The mortgage trigger restriction is significant. But if 25+ years in the data business have taught us anything, it’s that rule changes tend to force innovation forward, not backward.

The next phase of mortgage marketing will move up-funnel. Instead of waiting for a credit inquiry to react to, lenders will start identifying likely buyers earlier using signals like:

- Online home search behavior and digital research activity

- Equity and affordability signals from property and financial data

- Life-stage and financial indicators—marriage, growing families, career changes

- Real-time predictive credit data that models readiness before a formal application

In other words: predict intent instead of reacting to it.

Monitor360 is already built around this approach. With 100+ trigger types spanning credit, property, life events, and consumer behavior signals, lenders can identify emerging homebuyers weeks or months before they formally enter the market. The lenders who win in the next cycle won’t be the fastest dialers. They’ll be the ones who know who’s entering the market before everyone else does.

Measuring What Matters

Success in trigger marketing comes down to three metrics:

Speed to Contact

How quickly do you reach triggered consumers after their inquiry? Industry data consistently shows that contact within 24 hours dramatically outperforms slower responses.

Response Rate

Are your offers resonating? Financial services direct mail averages 3.95%, but well-executed trigger campaigns regularly achieve 4-6% or higher.

Conversion Rate

Response is one thing; conversion is what pays the bills. Pre-screen trigger campaigns typically convert at 10-15%, compared to 2% for generic digital leads.

Track these metrics by trigger type, channel, and offer. You’ll quickly identify which signals drive the highest-value opportunities for your specific products.

Getting Started

If you’re currently relying on purchased lead lists or aging CRM data, the shift to trigger-based marketing represents a fundamental change in how you find and engage prospects.

Start by identifying your highest-value use cases:

Portfolio Protection

Monitor your existing customers for signals they’re shopping with competitors. This is often the highest-ROI application since retaining a customer costs far less than acquiring a new one. With mortgage triggers now restricted, portfolio monitoring is the most direct path to identifying existing customers who are in-market.

New Customer Acquisition

Focus on trigger types that align with your core products. If you’re strong in VA loans, VA loan inquiry triggers should be your starting point.

Cross-Sell Opportunities

Use property and life event triggers to identify existing customers who may need new products – homeowners with significant equity for HELOCs, new movers for auto loans.

The most successful programs don’t try to monitor everything at once. They start focused, prove ROI on a specific trigger type, then expand from there.

The Speed Advantage

In direct marketing, response rates are important. But in trigger marketing, speed is everything.

A consumer who filled out a mortgage application yesterday is 10x more valuable than someone who did so last month. They’re making decisions now, comparing offers now, and choosing a lender now.

Financial services companies were anticipated to increase direct mail volumes from 48.3 million pieces in 2024 to 69 million in 2025—a 43% boost. And for 2026, according to the ABA, nearly 1 in 4 bank marketers report that they are maintaining or increasing their investment in direct mail heading this year, underscoring the channel’s continued importance in financial services marketing.

That growth is being driven primarily by lenders who understand that timely, targeted outreach outperforms generic batch campaigns.

The question isn’t whether to use trigger data – it’s whether you can afford to keep sending offers to people who made their decision weeks ago while your competitors reach them within 24 hours.

About Monitor360 by Altair Data

Altair’s Monitor360 delivers unified credit and consumer alerts with less than 24-hour turnaround on over 100 trigger types—from credit inquiries to life events to property signals. Designed for financial services marketers who need to act fast without sacrificing compliance or data quality. Altair Data is a leading provider of credit and consumer intelligence for financial services organizations. We help lenders and marketers make faster, smarter, and more compliant decisions. To learn more about our solutions, get in touch with us.