A set of converging pressures is fundamentally reshaping the consumer lending environment in 2026 — and with it, how credit products get marketed.

Interest rates remain elevated compared to pre-pandemic levels. Credit card balances have climbed past $1.2 trillion. Delinquencies are inching up. Underwriting is cautious. And consumers are taking a closer look at how they manage debt.

So now, every campaign dollar faces more scrutiny than it did two years ago.

The instinct in this environment is to pull back: mail fewer pieces, run fewer campaigns, wait for conditions to improve. But the lenders and credit unions gaining market share right now are doing the opposite. They’re not spending more. They’re targeting more precisely — using richer data, smarter segmentation, and faster activation to shrink their mailing universe on purpose and actually improve ROI in the process.

The difference between a profitable prescreen campaign and a money pit often isn’t creative, channel mix, or offer structure. It’s the quality and depth of the data behind the list. And in 2026, that gap is widening fast.

The Hidden Tax on Thin Data

Most lender marketers understand that prescreen data — credit bureau data used to build lists of consumers who meet specific underwriting criteria — is the backbone of acquisition marketing.

What fewer teams fully appreciate is how much audience they leave on the table by relying on a single credit bureau as their data source.

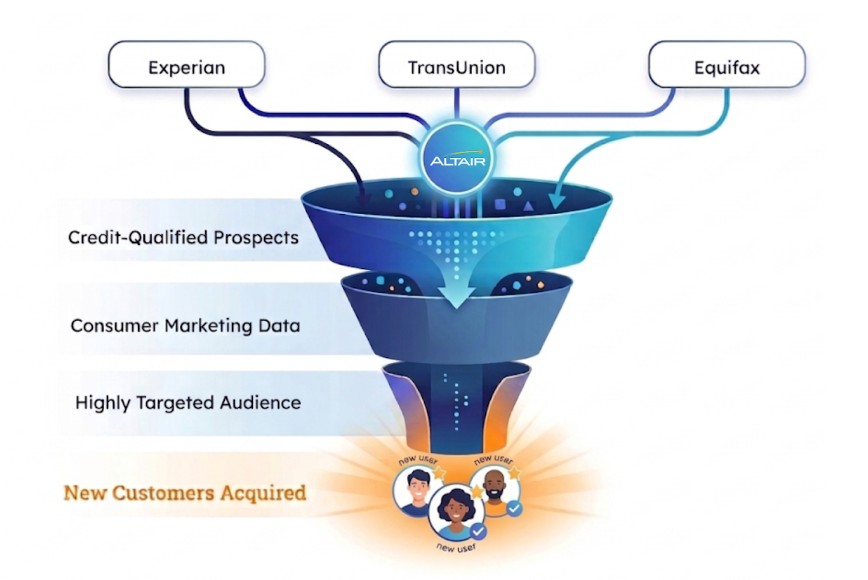

Each bureau — Equifax, Experian, and TransUnion — maintains its own database, drawing from its own network of reporting creditors. The overlap is significant, but not complete. One bureau may carry a tradeline that another completely misses. An inquiry one bureau captures may never surface on the other two.

In practical terms, relying on a single bureau for your prescreen campaigns means you’re structurally missing 20–40% of your addressable market before you even select a single filter or apply a single credit criterion. That’s not a rounding error. It’s a coverage gap that compounds across every campaign you run.

And the cost isn’t just fewer names on a list.

When your qualified universe is artificially smaller, your fixed costs — creative development, compliance review, print production, postage, analytics — get spread across fewer convertible prospects. Your cost-per-acquisition rises, your response rates look softer, and your campaign economics deteriorate. Not because your strategy was wrong, but because your data didn’t give you a complete picture of the market.

Tri-bureau credit data solves this structurally. By merging data from all three bureaus into a single, deduplicated view, you gain access to the full credit-active consumer universe. The lift is real and consistent: lenders using tri-bureau data routinely see a 20%+ increase in qualified prospect volume over single-bureau campaigns and a 50% or greater lift in trigger-based programs.

Credit Data Alone Isn’t Enough Anymore

Expanded bureau coverage gets you a bigger, more complete pool of qualified consumers. But in the consumer lending market where every lender with a prescreen contract has access to credit data in some form, coverage alone isn’t a competitive advantage. The real edge comes from what you layer on top of it.

The lending marketers outperforming their peers in 2026 are combining credit qualification with consumer, behavioral, and life-event data. The goal is to build segments that are both credit-eligible and contextually ready to act.

Think about the difference between mailing everyone with a 720+ FICO in a geography versus reaching a much smarter subset. Consumers who recently searched for auto loans online. People who just moved, got married, or show behavioral signals that correlate with conversion.

That’s the real edge.

This is what “smarter segmentation” actually means in practice. It’s not just tighter credit filters. It’s a fundamentally richer data foundation that lets you:

- Identify in-market consumers using real-time credit inquiry triggers — not just static snapshots

- Layer 1,000+ consumer attributes (demographics, lifestyle, financial signals, property data, digital shopping behavior) onto credit-qualified audiences

- Build predictive models that rank prospects by likelihood to convert, not just likelihood to qualify

- Suppress existing customers, opt-outs, and low-probability records before you spend a dollar on production or postage

When credit data and consumer intelligence live in the same platform — accessible through the same query, applied to the same record — you stop making tradeoffs between qualification and intent. You get both. And that’s where campaign economics start to shift meaningfully in your favor.

Speed Is the Multiplier Most Teams Undervalue

Even with the right data, there’s a second variable that separates high-performing campaigns from average ones: activation speed.

Fintech Market’s 2026 consumer lending analysis identifies real-time decisioning as a defining shift. Lenders are using automated decision engines to pre-approve or soft-approve consumers inside marketing funnels, collapsing the gap between “ad impression” and “credit decision.”

The same principle applies to prescreen campaigns: the faster you move from data pull to live campaign, the more demand you capture.

In a traditional managed-service model, building and launching a prescreen campaign follows a predictable but slow sequence. Submit a data request. Wait for your vendor to pull and process the list. Review and approve. Coordinate with your mail house or digital partner. Then launch.

That cycle can take weeks.

In a competitive lending market, weeks are an eternity. A consumer who triggers today may close with a competitor within days.

The alternative — self-serve platforms where marketing teams access tri-bureau credit and consumer data directly, build audiences in real time, and export campaign-ready files same-day — compresses that cycle from weeks to hours.

Thousands of lender marketers already rely on platforms serving 250 million+ consumer records with 1,000+ attributes.

For teams with deeper technical resources, API-driven access takes this further. Rather than logging into a platform to manually pull lists, an API integration gives you full programmatic control.

Query Credit and Consumer Data on Demand

Manage persistent audience catalogs that update in real time — no more static flat files that go stale. Process records individually or in batch. Push results directly into your CRM, LOS, or campaign management system.

Response times measured in milliseconds, not business days.

The compounding effect of speed is significant. When you can test a new segment on Tuesday and have results by Friday, you iterate faster. When you can react to a rate change or competitive move within hours instead of weeks, you capture demand your competitors miss. Speed doesn’t replace strategy, but it makes good strategy dramatically more productive.

What Financial Services Marketing Teams Should Look for in a Data Partner

If you’re evaluating data providers for prescreen, trigger, or enrichment campaigns, the questions that matter most aren’t the ones on the typical RFP template. Yes, you need to confirm bureau access, data freshness, and compliance posture. But the questions that actually predict campaign performance and long-term partnership value are more operational:

- Can you access credit and consumer data in the same environment, or do you need separate partners, separate contracts, separate platforms, and separate timelines for each?

- Is the platform self-serve, or are you dependent on a managed-service team for every list pull? Both models have a place — but you should know which one you’re buying.

- How fast can you go from signed contract to first live campaign? If the answer is “60–90 days,” that’s a signal about the platform’s operational maturity.

- Is there an API option for teams that want to integrate credit and consumer data directly into their own systems? And if so, is it well-documented, with real developer support — not just a PDF spec sheet?

- What does ongoing campaign support look like? Matchback reporting, A/B test tracking, predictive modeling, and optimization should be part of the conversation, not a separate SOW.

The right data partner isn’t just a list vendor. They’re an operational extension of your marketing team, one that gives you better data, faster access, and built-in compliance so you can focus on strategy, creative, and conversion.

Where Are Credit-Focused Marketers Heading

The lending marketers seeing the best results in 2026 aren’t the ones with the biggest budgets.

They’re the ones with the most complete view of their market, the most precise segmentation, and the shortest distance between data and action.

Tri-bureau credit data gives you the foundation: full market coverage, accurate qualification, and the lift that comes from seeing what single-bureau sources miss. Layering consumer intelligence on top turns that foundation into a targeting engine. And self-serve or API-driven access turns that targeting engine into a speed advantage your competitors can’t easily replicate.

Better segmentation. Faster activation. Smarter spend. That’s not a budget conversation. That’s a data conversation.

Ready to see what smarter segmentation looks like for your next campaign? Transform your financial services marketing with smarter data.

>> Talk to a data strategist at Altair

Frequently Asked Questions

What is FCRA compliance in lending marketing?

The Fair Credit Reporting Act (FCRA) governs how consumer credit data can be used in marketing. For lenders, this means prescreen campaigns must follow strict rules — including offering consumers a firm credit offer and honoring opt-out requests. Working with a data partner that builds FCRA compliance into its workflows removes this burden from your internal team.

What is prescreen marketing?

Prescreen marketing is a credit-based targeting method where lenders use bureau data to identify consumers who meet specific underwriting criteria before making a credit offer. It’s one of the most precise acquisition tools available — but only as effective as the data behind the list.

What is tri-bureau credit data?

Tri-bureau credit data combines consumer credit information from all three major bureaus — Equifax, Experian, and TransUnion — into a single deduplicated view. Because each bureau maintains its own database, using all three gives lenders a significantly more complete picture of the credit-active consumer market.

How does consumer data improve lending campaigns?

Layering consumer attributes — such as demographics, lifestyle signals, and life events — onto credit-qualified audiences allows lenders to target people who are both eligible and contextually ready to act, improving conversion rates without increasing spend.