You’re launching a prime auto loan campaign. Your data vendor delivers 10,000 qualified prospects. Launch day arrives, your offer goes out, and responses trickle in below forecast.

Three weeks later, a competitor running the same campaign with the same offer reports 15,000 qualified prospects and substantially better response rates. How did they pinpoint an additional 5,000 qualified prospects that you completely missed?

The answer: Tri-bureau credit data.

The Coverage Problem Most Marketers Don’t Know They Have

Credit reporting in the United States operates through three major credit bureaus: Equifax, Experian, and TransUnion. Most financial marketers understand this. What they don’t always realize is that accessing data from just one bureau means seeing only a fraction of your addressable market.

Here’s why: Not every creditor reports to all three bureaus.

Many lenders, credit card issuers, and financial institutions have reporting relationships with only one or two bureaus. This creates a coverage gap that single-bureau marketing programs never see.

When someone applies for a mortgage, that inquiry might appear at Experian within hours—but not show up at TransUnion for 48 hours, or at Equifax at all. If you’re only monitoring one bureau, you’re missing opportunities your competitors are capturing in real-time.

The practical impact? Tri-bureau access can reveal 30-50% more qualified prospects compared to single-bureau programs. That’s not theoretical lift—that’s actual addressable market you’re leaving on the table.

New to Credit-Based Marketing?

Credit bureau data powers some of the most effective marketing strategies in financial services:

- Prescreen campaigns: FCRA-compliant firm offers of credit sent to pre-qualified consumers

- Credit triggers: Real-time alerts when consumers apply for loans or credit

- Propensity modeling: Predictive models identifying who’s likely to respond or convert

- Portfolio monitoring: Tracking existing customers for cross-sell opportunities or churn risk

- Suppression: Ensuring you don’t market to unqualified consumers

Unlike consumer marketing data (demographics, interests, purchasing behavior), credit data shows actual borrowing behavior, payment history, and creditworthiness—making it essential for responsible lending and high-converting acquisition campaigns.

Why Credit Bureau Data Varies (The Short Version)

The three major credit reporting agencies don’t receive identical information. Here’s what creates the differences:

Reporting Relationships

There’s no legal requirement that creditors report to all three bureaus. Many regional banks, credit unions, and specialized lenders report to only one or two bureaus based on cost considerations and existing vendor relationships.

Timing Differences

Credit inquiries and account updates don’t hit all three bureaus simultaneously. One bureau might receive a mortgage inquiry on Monday, while another doesn’t see it until Wednesday. In trigger marketing where speed determines success, that 48-hour gap means your competitor got there first.

Data Completeness

A consumer with a robust credit file at Experian might have a thin file at TransUnion if their primary credit relationships don’t report there, leaving gaps in their credit history. This creates false negatives—qualified consumers who look unqualified because you’re viewing incomplete data.

Consumer Ecosystems

Different consumer segments tend to cluster around different bureaus based on their creditor relationships. Mortgage shoppers might be more visible at Experian, auto loan applicants at Equifax. Single-bureau programs miss entire consumer segments.

For marketers, this isn’t academic. It directly impacts who you can reach, when you can reach them, and whether your targeting criteria work as intended.

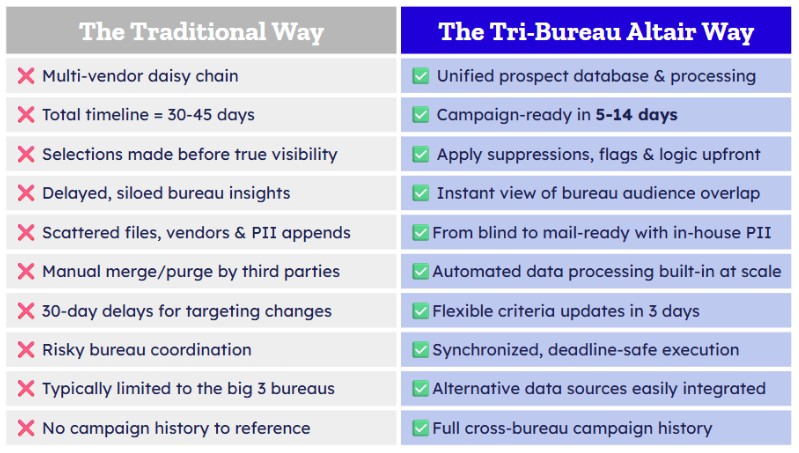

The Marketing Impact: What Single-Bureau Costs You

The chart speaks for itself. Legacy approaches to credit data processing create three core problems for modern marketers: incomplete coverage, operational delays, and coordination complexity.

Coverage Gaps You Can’t See

Single-bureau targeting creates two problems: missing qualified consumers with thin files at your selected bureau, and marketing to unqualified consumers who only look good in one bureau’s data. Tri-bureau processing solves both—you see the complete credit picture and make smarter targeting decisions.

Speed & Timing Issues That Kill Campaigns

Traditional credit data processing takes 30-45 days from list pull to campaign-ready data. By then, mortgage shoppers chose lenders, auto buyers purchased cars, and credit card prospects opened new accounts.

Unified tri-bureau data processing through an organization like Altair Data delivers campaign-ready data in 5-14 days and real-time triggers within hours. Criteria updates in 3 days instead of 30. When competitors wait for last month’s file, you’re reaching this week’s in-market shoppers.

The Workflow Penalty

Single-bureau programs create coordination nightmares: scattered files from different vendors, manual merge/purge by third parties, siloed bureau relationships with different SLAs, and no unified campaign history. Each touchpoint adds delay and error risk.

A unified tri-bureau platform eliminates this: one database, one processor, one relationship.

Automated deduplication prevents sending the same consumer multiple offers. Full cross-bureau campaign history shows which bureau drives best performance for each product type. That’s the type of streamlined, holistic reporting and analytics data-driven marketers dream of.

How Tri-Bureau Changes Your Marketing

Beyond just “more data,” tri-bureau access fundamentally changes what’s possible in credit-based marketing.

Tri-Bureau Coverage Reveals 30-50% More Qualified Prospects

A credit card issuer targeting prime consumers (FICO 720+) might get 50,000 qualified prospects from a single-bureau prescreen. Run that same campaign with tri-bureau data and see 70,000 qualified prospects—an extra 20,000 consumers with strong credit files at Bureau B and C but weak files at Bureau A.

Industry data consistently shows tri-bureau coverage lifts of 30-50% compared to single-bureau programs. For mortgage triggers, tri-bureau is even more critical—one bureau captures VA loan inquiries, another sees conventional applications, a third picks up HELOC shopping. Single-bureau programs could miss two-thirds of the signal.

Reduce Campaign Cycles from 30-45 Days to 5-14 Days

Financial services direct mail volumes are expected to jump from 48.3 million pieces in 2024 to beyond 69 million in 2026—a 43% increase driven by marketers discovering that timely, targeted outreach outperforms generic batch campaigns.

Tri-bureau platforms deliver campaigns in 5-14 days versus 30-45 day cycles from traditional vendors. For trigger campaigns, this means reaching consumers within 24 hours of their inquiry instead of 48-72 hours later after competitors already made contact.

Eliminate Duplicate Outreach with Cross-Bureau Deduplication

Without visibility across all three bureaus, the same consumer might receive your offer multiple times because they appear in different bureau files. This creates duplicate disclosure requirements, increased costs, and consumer confusion.

Tri-bureau platforms solve this automatically—see the same person across all three files, deduplicate before launch, and apply consistent business rules across your entire audience.

Multiple Integration Options: Platform, API, or Managed Service

Modern tri-bureau platforms offer multiple paths: self-serve platform access for on-demand list pulls, API integration (like Altair’s DataBridge solution) for programmatic access and CRM integration, or managed service with full campaign execution and strategic support. Start with platform access, add API when ready to automate, and tap strategic support for complex modeling.

Making Tri-Bureau Work Operationally

The conversation around tri-bureau typically starts with cost: “Won’t three bureaus cost 3x as much?”

Not necessarily. In fact, many marketers switching to unified tri-bureau platforms save 30-50% compared to their current multi-vendor arrangements.

Save 30-50% with Transparent Pricing vs. Hidden Multi-Vendor Fees

Traditional single-bureau programs include base bureau fees, third-party processing charges, QC and data hygiene fees, scoring and append costs, output variation charges, and manual merge/purge expenses. Add these up, and all-in cost per thousand often exceeds modern tri-bureau platforms like Altair—despite accessing only one bureau.

Unified tri-bureau platforms eliminate hidden fees through transparent pricing that includes processing, QC, scoring, and output variations. The comparison isn’t “three bureaus versus one”—it’s complete coverage with transparent pricing versus partial coverage with unpredictable costs.

Month-to-Month Agreements Replace Multi-Year Contracts

Legacy vendors also require multi-year contracts with minimum volume commitments.

Some modern tri-bureau platforms may even offer month-to-month agreements with 60-day notice, enabling you to prove ROI before scaling, adjust strategy based on results, and maintain negotiating leverage as your business grows.

Choose Your Integration Path: Self-Serve, API, or Full Cloud Integration

Start with platform-based list pulls for manual campaign execution. Add API access through DataBridge for automated workflows and integration with your marketing tech stack. Progress to native data sharing through cloud platforms like Snowflake with real-time trigger feeds and embedded analytics. The implementation path matters less than having options that support growth without massive upfront investment.

Phase Your Rollout: Prove ROI Before Full Conversion

Start with your highest-value campaign—mortgage acquisition, credit card prescreen, or auto triggers. Run tri-bureau against current single-bureau results. Measure coverage lift, response rate improvement, and cost per acquisition impact.

Once you’ve proven ROI, expand to similar programs. After proving performance across multiple campaigns, invest in deeper integration with API access and automated workflows. This staged approach minimizes risk, proves value quickly, and builds internal buy-in.

What to Expect: The Tri-Bureau Difference

When marketers switch from single-bureau to tri-bureau programs, three metrics consistently improve:

Addressable Market Size (+30-50%)

Significantly more qualified prospects than single-bureau programs deliver. Larger audiences enable better testing, improved segmentation, and stronger statistical confidence in performance metrics.

Campaign Velocity (60% Faster)

Cutting timelines from 30-45 days to 5-14 days enables more testing, faster response to market conditions, and capitalizing on seasonal opportunities. Real-time tri-bureau monitoring reaches consumers while they’re shopping—not after decisions are made.

Targeting Precision

Seeing complete credit across all three bureaus reduces false negatives (qualified consumers you miss) and false positives (unqualified consumers wasting budget). This precision shows up in response rates, approval rates, and cost per funded loan.

The Competitive Reality

Lenders using tri-bureau credit data see more opportunities, see them faster, and target more precisely than competitors with partial views. This advantage compounds over time—better targeting improves unit economics, faster campaigns enable more testing, expanded reach builds larger customer files.

The question isn’t whether tri-bureau matters—industry results prove it does. The question is whether your data strategy positions you as the lender who sees opportunities first, or the one who finds out after competitors have already won the business.

Moving Forward

Tri-bureau credit data reveals your complete addressable market, enables faster campaign execution, and often costs less than multi-vendor single-bureau arrangements through transparent pricing.

For financial services marketers evaluating data strategy, ask three questions: Does your current approach reveal your complete addressable market? Can you launch campaigns fast enough to capture real-time opportunities?

When you add all costs—bureau fees, processing, coordination, manual workflows—does single-bureau really cost less?

Modern tri-bureau platforms combine complete coverage with operational speed, transparent economics with technical flexibility, and strategic partnership with month-to-month accountability.

The result is marketing infrastructure that scales with your business rather than constraining it.

About Altair Data

Altair Data provides unified tri-bureau credit data and consumer insights designed for financial services marketers who need complete coverage, fast execution, and transparent pricing. Our platform includes DataBridge API access, self-serve campaign tools, and strategic support from teams who understand acquisition, triggers, and portfolio marketing. Get in touch with us to learn more about how we can help.